The Calm After the Storm: A Scammer's Opportunity

Here in Florida, we know a thing or two about hurricanes. The winds rage, the rain pours, and then, as quickly as it came, the storm passes. What's left behind is often a mess of downed trees, flooding, and damaged roofs. And right alongside the legitimate cleanup crews and trusted contractors, another kind of 'visitor' often arrives: the scammer. We've seen this play out hundreds of times – folks are vulnerable, desperate for a quick fix, and that's exactly what these predatory individuals or companies exploit.

A recent WFTV report highlighted this very issue, urging Floridians to be on guard. It's a critical message. Your home is your biggest investment, and after a hurricane, protecting it from further damage – and from fraudulent contractors – is paramount.

How Do Scammers Operate After a Storm?

These outfits are cunning. They know you're stressed, probably without power, and dealing with significant property damage. They capitalize on that urgency and emotional toll. Here are some of the most common tactics we've seen:

The "Storm Chaser" Tactic

- Unsolicited Offers: They literally chase storms. Right after a major event, unfamiliar trucks with out-of-state plates might show up uninvited at your door. They'll offer immediate repairs, often claiming to have noticed damage you weren't even aware of.

- High-Pressure Sales: They'll tell you that you need to act now, or your insurance claim will be denied, or that their 'special' price is only good for today. This is designed to prevent you from doing your due diligence.

- No Local Ties: Often, these companies have no established local presence. They pop up, do shoddy work (or no work at all), take your money, and then disappear, leaving you with more problems than you started with.

Demanding Upfront Payment and Shady Contracts

- 100% Upfront Payment: A major red flag. While a legitimate contractor might ask for a reasonable down payment (typically 10-30% for materials or to secure the job), demanding full payment before any work begins is a classic scam. Once they have your money, they might never return.

- Vague Contracts: If they offer a contract that's handwritten, lacks detail about the scope of work, materials, timeline, or total cost, walk away. A professional contract protects both you and the contractor.

- Offering to Handle Everything with Your Insurance: While a good contractor will help you understand the repair process relative to your insurance claim, be wary of anyone who insists on handling the entire claim process for you, especially if they ask you to sign over your insurance benefits (an Assignment of Benefits, or AOB). This can lead to inflated claims, disputes, and you losing control over your policy. Florida has specific laws regarding AOBs, and they can be complex.

Low-Ball Bids, Shoddy Work, or No Work At All

- Too Good to Be True Prices: If one bid is drastically lower than all the others, it's usually for a reason. They might use inferior materials, cut corners on labor, or simply plan to disappear after taking your deposit.

- Lack of Permits: Major repairs, especially roofing, often require permits from your local municipality to ensure the work meets Florida's stringent building codes. Scammers often skip this, leaving you liable for fines and costly rectifications later.

- Substandard Materials: They might promise high-quality materials but install cheaper, less durable alternatives that won't stand up to Florida's sun, humidity, or the next tropical storm.

How to Protect Your Home and Wallet

Don't let the urgency of hurricane damage cloud your judgment. Taking a few extra steps can save you a world of trouble and expense down the line.

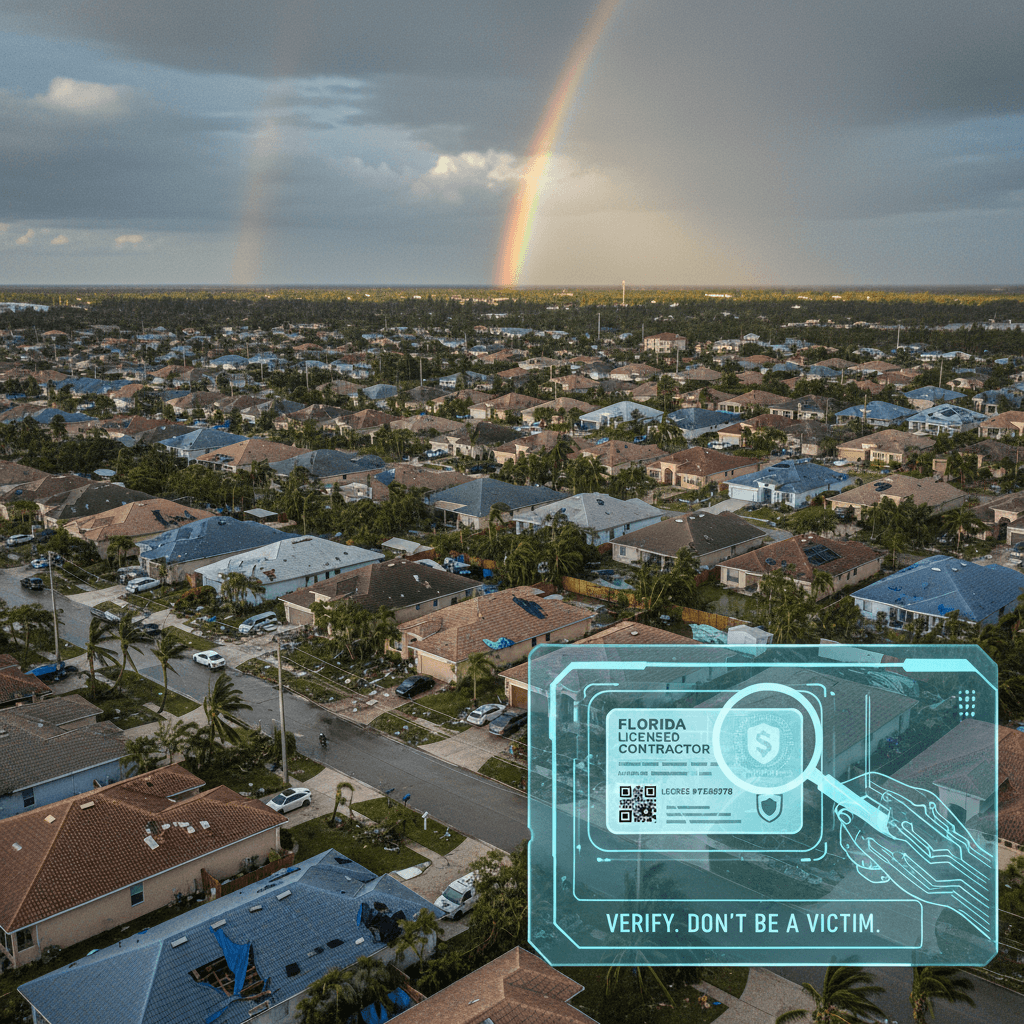

1. Verify Credentials and Licenses

- Check Licenses: In Florida, contractors must be licensed by the Florida Department of Business and Professional Regulation (DBPR). Ask for their license number and verify it online. Don't just take their word for it.

- Insurance: Ensure they have liability and workers' compensation insurance. Ask for proof, and even call their insurance carrier to verify coverage.

- Local Presence: Look for contractors with an established local address and a good reputation within the community. Ask for local references and check online reviews. The Better Business Bureau can be a good starting point.

2. Get Multiple Estimates (and detailed ones)

Don't jump on the first offer. Get at least three written estimates. Make sure each estimate clearly details:

- Scope of work.

- Specific materials to be used (brand, type, color).

- Payment schedule.

- Start and completion dates.

- Warranty information.

Comparing these apples-to-apples allows you to spot inconsistencies and avoid inflated pricing or suspiciously low bids.

3. Understand Your Insurance Policy and Claims Process

Before you even talk to a contractor, review your homeowner's insurance policy. Understand your deductible, what's covered, and your responsibilities. Work closely with your insurance adjuster. A reputable contractor will help you document damage and provide estimates for your adjuster, but they shouldn't try to dictate your claim or act as your adjuster.

4. Document Everything

Take extensive photos and videos of all damage before any repairs begin. Keep copies of all contracts, communications, invoices, and payment receipts. This documentation is crucial for your insurance claim and for any potential disputes with a contractor.

5. Be Wary of Door-to-Door Solicitors

While some reputable local businesses might canvass after a storm, be extra cautious with those who show up unsolicited, especially if they pressure you for an immediate decision or an upfront payment.

6. Never Pay for the Entire Job Upfront

Establish a clear payment schedule tied to the completion of specific stages of work. A common arrangement is a down payment, progress payments, and a final payment upon satisfactory completion of the entire project and passing all inspections.

The Krüger Difference: Your Local & Trusted Partner

Here at Krüger Disaster Recovery Team, we're not just contractors; we're your neighbors. We've lived through these storms, and we understand the stress and vulnerability you feel. That's why our priority is always to provide honest assessments, transparent communication, and top-quality repairs that adhere to Florida's rigorous building codes. We work with you and your insurance company to ensure your home is restored properly, safely, and without the headaches of dealing with fly-by-night operators.

When the storm clouds clear, make sure you're rebuilding with confidence. If you're facing hurricane damage and need a trustworthy team on your side, don't hesitate to reach out. We offer free inspections and straightforward advice to help you navigate the repair process.

Written by

Gus Kruger

CEO at Krüger

Gus Kruger is the founder and CEO of Krüger Disaster Recovery Team, a Florida-based company specializing in emergency property protection, roofing, and fencing. Since 2016, Gus has built the company from a one-man roof tarp operation into a full-service team of 50+ professionals, serving over 30,000 properties across Florida and the Southeast U.S. A preferred vendor for major insurance carriers, BBB A+ rated, and licensed & insured, Gus leads Krüger with a hands-on approach rooted in fast response, honest work, and long-term property solutions.