Navigating the Storm's Aftermath: What Your Insurer Expects in Florida

Here in Florida, we know hurricanes aren't just weather events; they're tests of resilience. As Gus Kruger, founder of Krüger Disaster Recovery Team, I've seen firsthand the chaos and confusion that follow a major storm. Property owners are often left scrambling, unsure of the first steps to take. And let me tell you, what you do (or don't do) in those crucial hours and days after the wind dies down can make or break your insurance claim.

Your insurance policy isn't just a piece of paper; it's a contract with specific obligations on your part, especially after a catastrophic event. Ignoring these can lead to denied claims, reduced payouts, and a whole lot of unnecessary headaches. We've helped hundreds of Florida homeowners navigate this exact situation, and in our experience, the key is proactive, informed action. Let's break down the five things your insurance company absolutely expects you to do after a hurricane, and what happens if you don't.

1. Prioritize Safety and Document EVERYTHING

First and foremost, ensure your family and property are safe. Once the immediate danger has passed, your very next step should be to document all damage. And I mean *all* of it. Get out your phone or camera and start taking photos and videos of everything – inside and out.

- Exterior Damage: Roof damage (missing shingles, exposed decking, damaged fascia), broken windows, compromised siding, downed fences, landscape damage.

- Interior Damage: Water stains on ceilings and walls, wet flooring, damaged personal belongings, mold growth (if you wait too long).

- Panoramic Shots: Don't just focus on the close-ups. Get wide shots that show the overall context of the damage.

Think of it like building your case. The more evidence you have, the stronger your position. Your insurer needs concrete proof of the damage caused by the storm. If you start making repairs without this initial documentation, you risk weakening your claim because the original damage won't be visible. The Federal Emergency Management Agency (FEMA) consistently advises thorough documentation for disaster recovery.

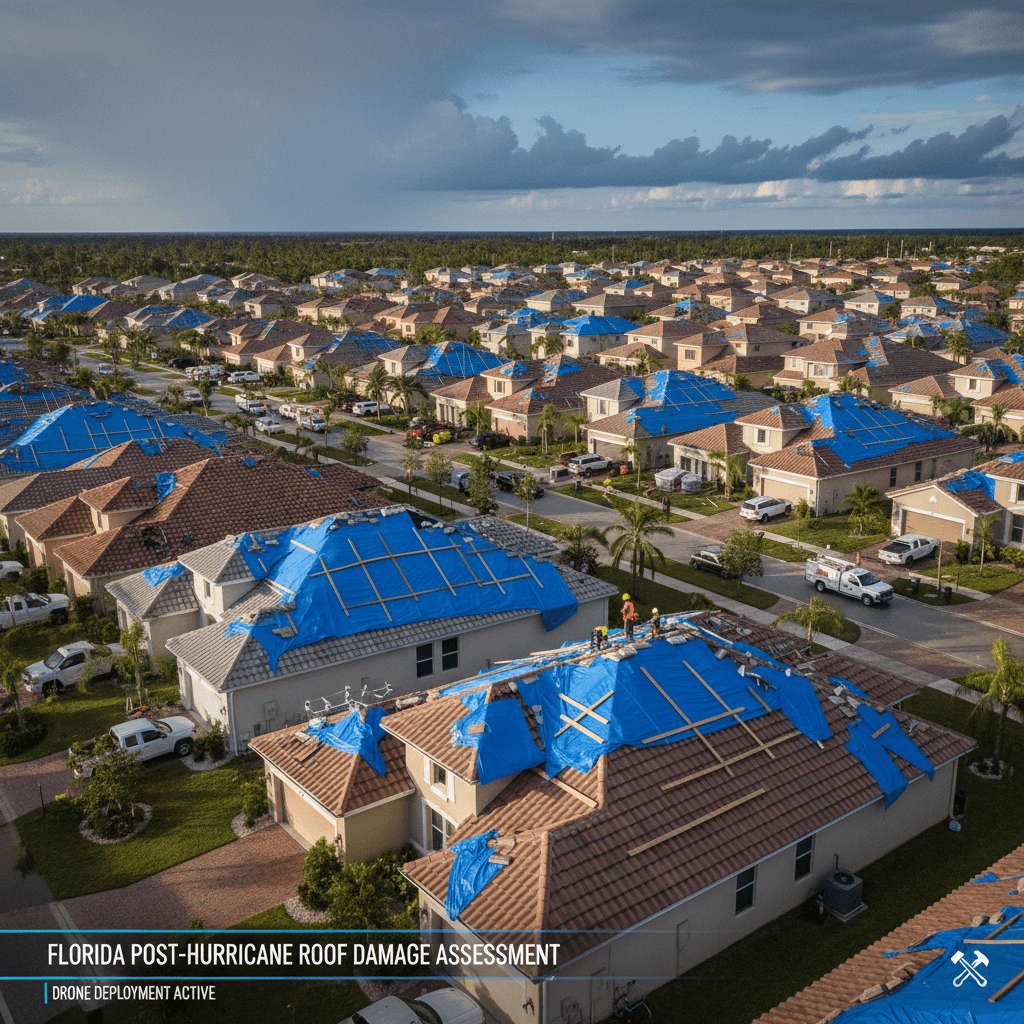

2. Mitigate Further Damage Immediately

This is a big one, and it's where many property owners unknowingly jeopardize their claims. Your insurance policy typically includes a clause requiring you to take reasonable steps to prevent further damage to your property. This means if your roof has a hole, you can't just let it sit there and allow rain to pour in, causing more extensive interior damage.

- Roof Tarps: If your roof is compromised, a temporary roof tarp is crucial. This is where our Krüger Disaster Recovery Team often steps in. We can quickly and securely tarp your roof, preventing water intrusion that leads to costly secondary damage like mold or structural issues.

- Board-Ups: Broken windows or doors should be boarded up.

- Water Extraction: If water has entered your home, you need to begin drying out affected areas to prevent mold growth.

Failing to mitigate further damage can result in your insurance company denying coverage for any damage that occurred *after* the initial storm, arguing you didn't fulfill your policy obligations. For instance, if a hurricane blows off shingles, and you don't tarp it, subsequent rain damage might not be fully covered. The Florida Department of Financial Services (DFS) emphasizes the homeowner's responsibility to prevent additional harm to their property.

3. Notify Your Insurer Promptly

Time is of the essence. Most policies require you to notify your insurance company “as soon as reasonably possible” or within a specific timeframe after the loss. Don't drag your feet on this. As soon as you've secured your property and documented the damage, call your insurer. Even if you're not sure how bad the damage is, it's better to get the claim started.

Delays can be problematic. Your insurer might argue that the damage wasn't reported promptly, making it harder to link it directly to the hurricane, or that the delay contributed to further damage (which they won't cover). While Florida law provides a significant window for hurricane claims, initiating the process quickly is always in your best interest.

4. Understand Your Policy and Deductible

Before you even make that call, or at least before the adjuster arrives, take some time to review your actual insurance policy. It's a dense document, but knowing a few key things will empower you:

- Hurricane Deductible: In Florida, hurricane deductibles are common and are often a percentage of your dwelling coverage (e.g., 2% or 5%). This is separate from your standard deductible. Understanding this helps manage expectations about out-of-pocket costs.

- Coverage Types: Know if you have actual cash value (ACV) or replacement cost value (RCV) for your roof and personal property. RCV typically pays for the cost of a new roof, while ACV factors in depreciation.

- Endorsements: Are there any specific endorsements that might apply to hurricane damage, like extended replacement cost?

Knowing what your policy covers will help you speak confidently with your adjuster and ensure you're getting what you're entitled to. The Florida Office of Insurance Regulation (FLOIR) offers valuable resources for understanding policy nuances.

5. Prepare for the Adjuster and Get Professional Assessments

Once you've filed your claim, an insurance adjuster will be assigned to assess the damage. This is their job – to evaluate the extent of the loss and recommend a payout. However, their assessment might not always align with the full scope of damage, especially for something as complex as a roof.

This is where professional assistance becomes invaluable. Before the adjuster's visit, consider having a reputable, local contractor like Krüger Disaster Recovery Team conduct an independent assessment. Our Ladder Assist service means we'll get up on your roof, meticulously document all damage, and provide a detailed estimate. This ensures that when the adjuster arrives, you have a professional report to compare against their findings.

We can walk through the property with the adjuster, pointing out damage they might overlook and advocating on your behalf. Our goal is to ensure your claim accurately reflects the damage and secures the funds needed for proper roofing repairs or replacement, meeting Florida's stringent building codes, which often requires a full roof replacement even for localized damage if a certain percentage is affected.

What Happens If You Don't Follow These Steps?

Ignoring these expectations can have severe consequences:

- Claim Denial: For serious policy breaches, like failing to mitigate damage, your entire claim could be denied.

- Reduced Payouts: Your insurer might only cover the initial damage, not the subsequent damage you could have prevented.

- Delayed Process: Lack of documentation or untimely reporting can significantly prolong the claims process.

- Out-of-Pocket Expenses: Ultimately, you could be left paying for repairs that should have been covered.

Navigating hurricane recovery in Florida is tough enough without the added stress of insurance claim issues. At Krüger Disaster Recovery Team, we're here to be your trusted partner, from securing your property with a tarp to assisting with the complex claims process and ultimately restoring your home. Don't let a hurricane leave you vulnerable twice.

If your Florida property has been impacted by a storm, reach out to us today for a free, no-obligation damage assessment. We'll help you understand your options and ensure you're on the right path to recovery.

Written by

Gus Kruger

CEO at Krüger

Gus Kruger is the founder and CEO of Krüger Disaster Recovery Team, a Florida-based company specializing in emergency property protection, roofing, and fencing. Since 2016, Gus has built the company from a one-man roof tarp operation into a full-service team of 50+ professionals, serving over 30,000 properties across Florida and the Southeast U.S. A preferred vendor for major insurance carriers, BBB A+ rated, and licensed & insured, Gus leads Krüger with a hands-on approach rooted in fast response, honest work, and long-term property solutions.